Table of Content

That noted, as with so many things, the coronavirus pandemic has impacted the availability of FHA loans, with some lenders having tightened their qualifications for approval. While the Department of Housing and Urban Development ultimately sets the ground rules for these types of loans, some lenders add their own specific conditions. As such, there may be differences in eligibility requirements from lender to lender.

Compared to a conventional loan, one that the government does not guarantee, an FHA loan has fewer requirements. You'll need a better credit score, a lower debt-to-income ratio and a larger down payment to qualify for a traditional loan. As you can see, there is a broad group of people who can qualify for an FHA loan to buy a house.

What's Your Property Worth?

FHA loans require that buyers make a down payment of at least 3.5 percent against the purchase price, or $3,500 for every $100,000. In fact, first-time buyers make up the majority of applicants who use this program. It’s a popular financing method among this group, partly due to the 3.5% down payment. Opinions expressed here are author's alone, not those of any bank, credit card issuer or other company, and have not been reviewed, approved or otherwise endorsed by any of these entities. All information, including rates and fees, are accurate as of the date of publication and are updated as provided by our partners.

This is how it is possible for FHA loan providers to hand out such great loans for people with less than ideal financial qualifications. First, let's talk about one of the most common types of home loans - conventional loans. Conventional loans are often sought after because they provide fixed, low-interest rates. However, they are some of the most difficult loans to obtain. While the phrase "FHA loan" is often used to describe a single type of mortgage, the FHA actually offers a variety of loan products and programs. This includes everything from loans that bundle rehabilitation or energy-improving expenses into a mortgage to loans for specific populations such as Native Americans and Native Hawaiians.

What to get the person who has everything — except a mortgage payment?

If you can’t afford to put 10% down on a home loan, the FHA will allow you to qualify with as little as a three-percent down payment. You can only use an FHA loan to buy a home you plan to use as your primary residence because the FHA program is intended to encourage primary homeownership. If you want to purchase a vacation home or investment property, you’ll need to check out othertypes of home loans. Certain duplexes and condominium buildings with up to four units are eligible for FHA loans.

Plus, mortgage rates can be very different from bank to bank. When you apply for an FHA loan with us, our team will go to work to help you find the best rates available to you. Well discuss each type of FHA loan, what the qualifications are, and help you understand the options available based on your unique situation. FHA loans help you buy a home with limited credit or a reduced down payment. Learn how to qualify for an FHA loan and what to expect when you apply. Aside from incredibly attractive interest rates, VA loans can be obtained with zero money down.

Boost Your Credit First

Once approved, the inspector is paid to perform the inspection. The minimum home inspection to qualify for FHA financing is $400. In this case, an FHA mortgage may simply not be an option and you’ll have to consider other loan types. For example, a 5% down conforming conventional loan has less stringent property requirements than FHA. This type of home loan may require higher FICO scores and may be limited to single-unit residences. First-time buyers want to know how much theyre expected to save for their FHA loan down payments.

They are similar to USDA loans in that they do not require a down payment or mortgage insurance. They offer competitive interest rates and have more lax requirements than conventional mortgages. Borrowers generally have to be veterans who have served for certain lengths of time or under specific circumstances. FHA loans can be great for first-time homebuyers as they may qualify for a down payment as low 3.5% of the purchase price. And people with lower incomes and credit scores may also qualify for FHA loans.

Can I use my equity to buy another house?

If a conventional loan is within your reach, it's worth comparing both the short-term and long-term costs since FHA mortgage insurance premiums can add up. Lenders review your credit report and scores as part of the mortgage application process to assess your creditworthiness and adjust loan terms accordingly. If you have a FICO score of 580 or higher, you might be eligible for an FHA loan with only 3.5% down. You could still qualify for an FHA loan if your FICO score is as low as 500, though it requires a larger down payment of 10%. To see where your credit stands, you can check your credit report for free through Experian. Many types of properties are eligible for the FHA financing program.

An adjustable-rate mortgage, known as an ARM, features a low rate for an introductory period. After the initial period, the rate can change based on a number of financial indices. Though there are thresholds for how high or low the interest rate can go, ARM payments are likely to fluctuate over the lifetime of the loan. If you meet the requirements for both an FHA loan and a conventional loan, take time to compare total costs. You can use our mortgage loan calculator to help see which loan will better serve your financial needs. A fixed-rate mortgage is a mortgage where your interest rate is fixed for the entire term of your loan.

The appraiser will observe whether the habitable rooms have a functioning heat source and whether the property has sufficient electricity to feed all the home's lights and electrical systems. A property can fail inspection if the appraiser observes damaged or frayed electrical wires. The FHA can refuse to insure a loan if the home shows signs of structural damage. Red flags include defective construction, hazardous materials, leaking pipes, dampness, decay, standing water, termite damage and continuing settlement. The FHA is not worried about cosmetic defects that do not affect the safety, security or soundness of the home.

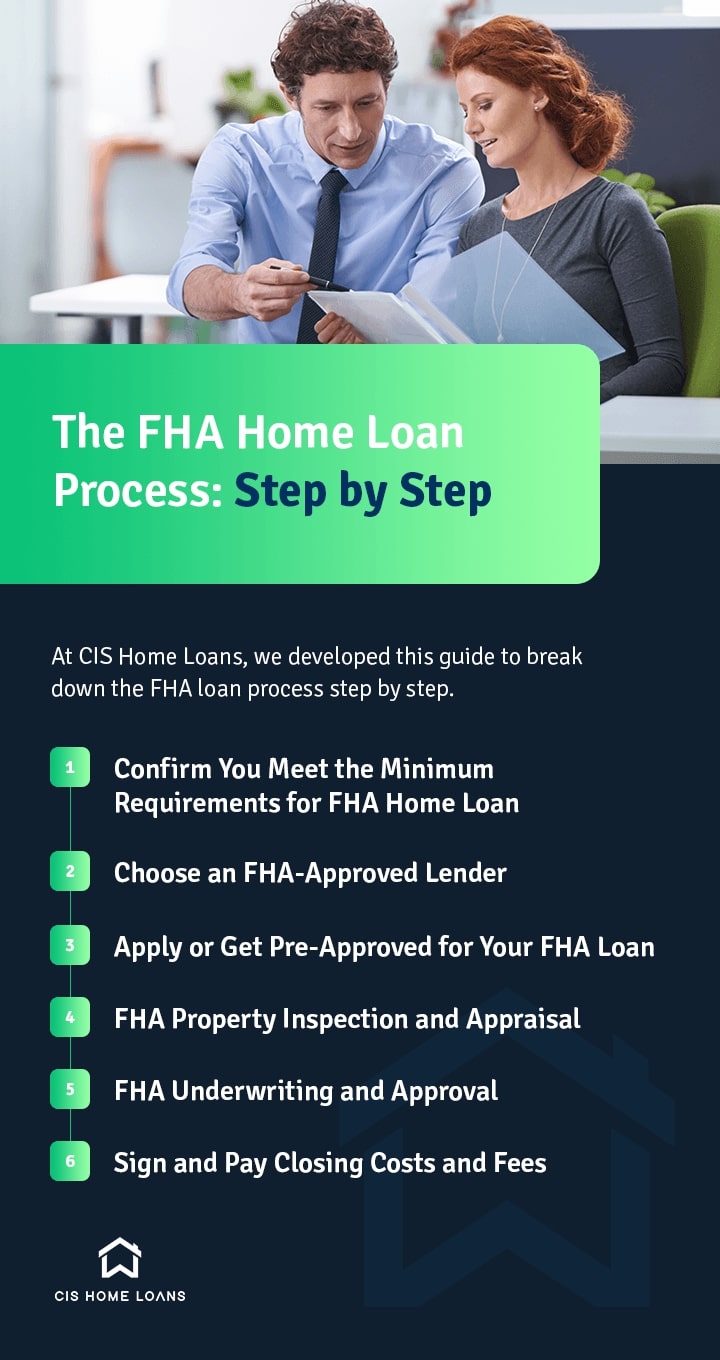

You get an FHA loan from a private lender, just like you would a conventional loan. FHA loans must accompany homes that an FHA appraiser has evaluated. The inspection sees if the home will meet Housing and Urban Development standards. If the home does not adhere to HUD property guidelines, you will not be able to get an FHA loan for it. You can use our home affordability calculator to see approximately how much house you can qualify for.

FHA loans have been helping people become homeowners since 1934. The Federal Housing Administration - which is part of HUD - insures the loan, so your lender can offer you a better deal. These types of mortgages, called FHA 203 loans, are also available as a refinancing loan according to the FHA official site. The FHA requires a minimum home inspection before approving a loan. The home inspection is a critical step in the process because it ensures that the property’s overall structure is safe.

Borrowers should have a manageable level of debt, as determined by the debt-to-income ratio and other factors. Whether you are shopping for a car or have a last-minute expense, we can match you to loan offers that meet your needs and budget. Hearst Newspapers participates in various affiliate marketing programs, which means we may get paid commissions on editorially chosen products purchased through our links to retailer sites. They will look for any problems with the building, such as frayed wires or damaged countertops. However, they will not be enough to prevent the property from passing the FHA appraisal. Another critical factor is whether there are good access points for pedestrians and emergency vehicles.

What is the debt-to-income ratio for a second home?

The lender will then sell the house as a way of reclaiming as much of the money still owed on the loan as possible. For customers with a credit score of less than 680, FHA rates are usually cheaper than conventional rates. The influence of credit score on mortgage rates is greater than the impact of loan type.

No comments:

Post a Comment